The energy sector is developing rapidly. The process of European market integration began some years ago. Its purpose is to create a single European market that enables market parties to trade gas and electricity across national borders easily and efficiently.

Electricity market

Transparency data

We provide transparency data on our operations on our Dutch and German transparency page and on ENTSO-E.

To transparency pagesEuropean target model

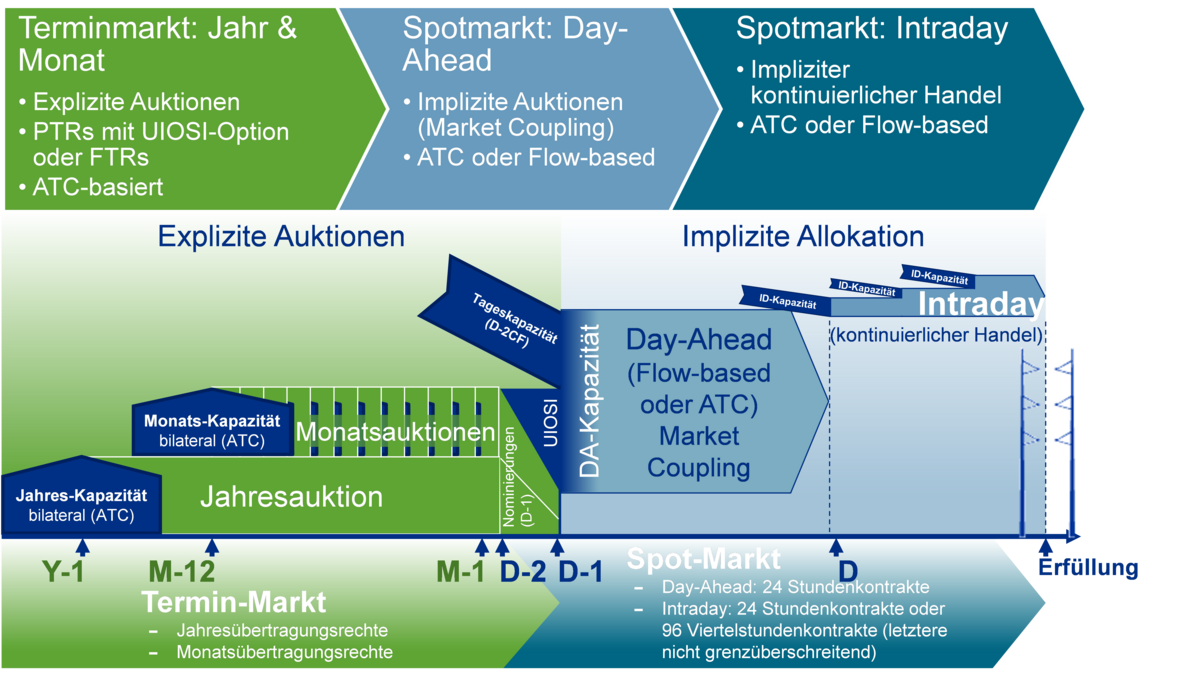

The European Norm includes both the explicit allocation of transmission capacities in the form of annual and monthly transmission rights (derivatives market) as well as the implicit allocation in the day-ahead and Intraday markets (spot market).

Spot market

Day-Ahead Market Coupling

Day-Ahead Market Coupling has been introduced in Europe gradually or by expansion. Between 2006 and 2010 the Day-Ahead markets of France, Belgium and the Netherlands were connected into the "Tri-lateral Market Coupling”. In 2010, as part of the market harmonisation, the association of day-ahead markets of the CWE region was created1. At the same time, a volume coupling was generated between the CWE and the Nordic region.

In February 2014, there was a big step toward European market integration, when the market coupling in the NWE region2 was put into operation. Price coupling was expanded into further countries in the following years (e.g. Spain, Portugal and Italy) and was renamed to Multi Regional Coupling (MRC).

Implicit Continuous Intraday Coupling

In Intraday markets, the participants have the opportunity to react to changes in production or consumption up until shortly before the time of delivery. This is of particularly great importance against the background of a growing proportion of fluctuating supplies from renewable energy sources, because production cannot always be forecast sufficiently well. Therefore, the European Norm has planned a continuous implicit trade for the intraday time-frame. In the fall of 2013, the TSO and the energy exchanges approved a pilot project for the NWE region with the aim of implementing a Cross-Border Intraday Market Project, or short: XBID). The project is to build a central system for continuous, implicit intraday electricity trading. The pilot project is to begin its operation in Q3/2017.

1Central Western Europe: Belgium, Germany, Austria, France, Luxembourg, the Netherlands.

2North Western Europe includes the CWE region, Scandinavia, Great Britain and the Baltic States.

Derivatives Market

Auctioning off of long-term transmission rights

Long-term transmission rights are rights over a duration of one week and up to one year. The most common are annual and monthly transmission rights. As a rule, these are directionally fixed rights, divisible by MW. In principle, there are purely financial rights, the so-called Financial Transmission Rights (FTR) as well as “real” transmission rights, the so-called Physical Transmission Rights (PTR), which really are only entitled to the nomination of cross-border schedules.

Most PTRs also have a so-called “Use-It-Or-Sell-It“ (UIOSI) component, which has the consequence of having to payout the resale value if the transmission rights have not been exercised by registering a schedule. An FTR is always followed by the payout of the resale value and does not contain the right to register a schedule.

The resale value of both type of rights is derived from the day-ahead allocation of the returned capacity. In the case of explicit auctions, the payout corresponds to the auction price of the respective hour, in the case of the day-ahead market coupling (EU Norm), dispersements correspond to the hourly price differences of the day-ahead power auctions of the two bidding zones, in the appropriate direction, as long as this is greater than zero (!). FTRs as well as PTR with UIOSI are therefore swaps dependent on the directional and favourable hourly day-ahead price differences. The payout for a transmission right for A→B equals ∑h MAX{0;PB,h - PA,h}.

The owner of the rights will, against payment of the auction price and for the respective period of one year or one month, receive the payout from the TSO for the hourly price differences at the day-ahead power auction between the two bidding zones, as long as these are positive. In addition, PTR along with UIOSI also have the option to register a schedule. The Strike Price of the option is dynamic and corresponds to the above mentioned resale value. However, this is not known at the time of the strike. Therefore, it is usually not of an advantage to exercise this option and the strike price is very low.

Schematic representation of the European target model